TL;DR — On 5 February 2018, inverse-volatility ETPs lost ~$3 billion in 50 minutes. XIV — a Credit Suisse ETN — went from $108 to $4. It was not a freak event; it was the latest instance of a reflexive-hedging blow-up that happens every 3–4 years. A LASSO-regression stop — Example 8 from my book Hands-On AI Trading with Python, QuantConnect and AWS — would have flattened the position hours before the cliff. I re-ported the algorithm to C# on QuantConnect, ran three backtests side-by-side, and the equity curve tells the story.

1. Executive summary

- The product: XIV — VelocityShares Daily Inverse VIX Short-Term ETN, issued by Credit Suisse AG (Nassau branch), ticker XIV, CUSIP 22542D506. Launched 29 Nov 2010. Terminated 21 Feb 2018.

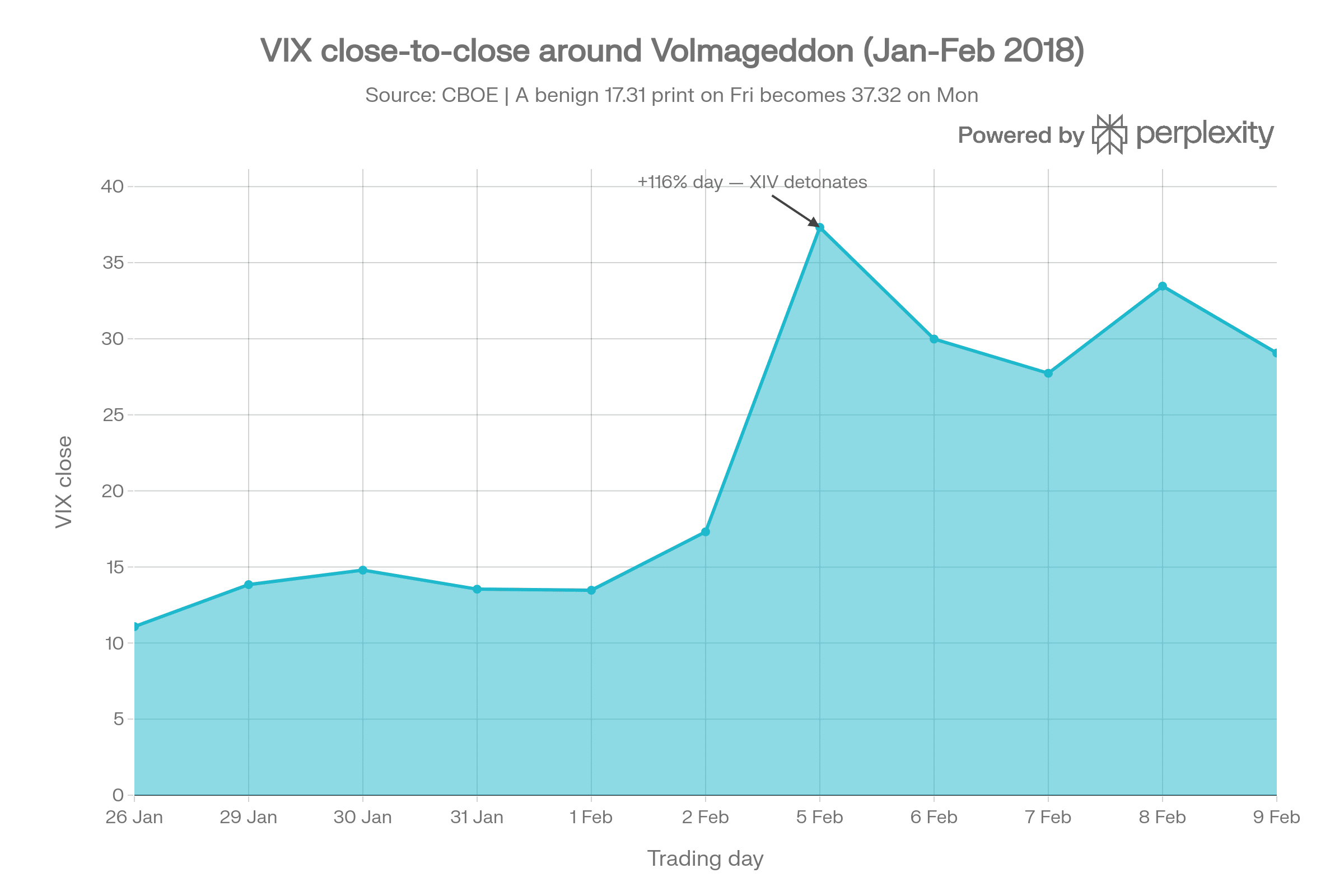

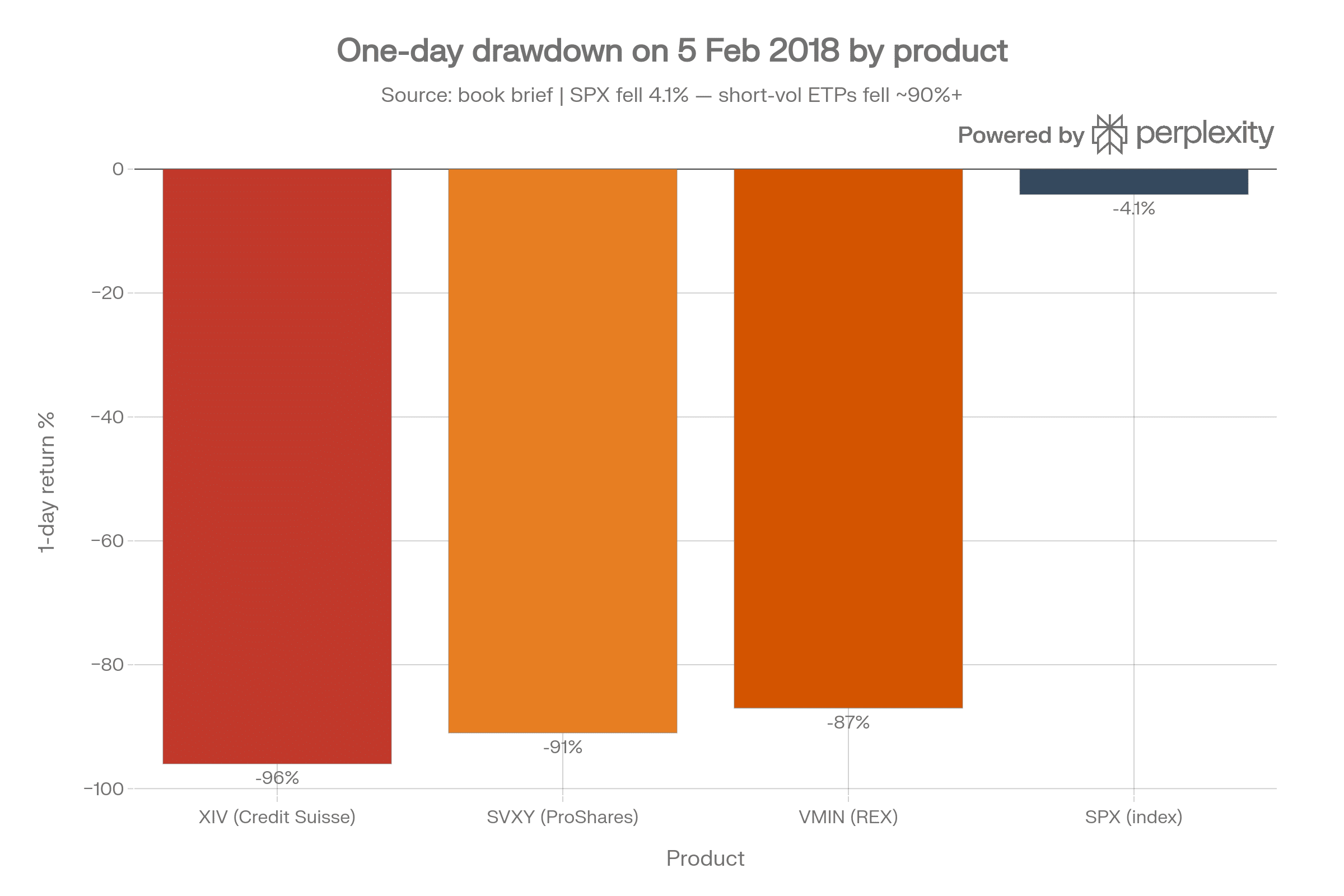

- The event: 5 Feb 2018. VIX +116%. XIV −96%. SVXY −91%. VMIN −87%. S&P 500 only −4.1%.

- The pattern: Reflexive-hedging blow-ups happen roughly every 3–4 years across different wrappers. Same machine; different paint job.

- The fix: Chapter 6, Example 8 — a LASSO-regression dynamic stop on {VIX, ATR(22), σ(22)} → weekly-low return.

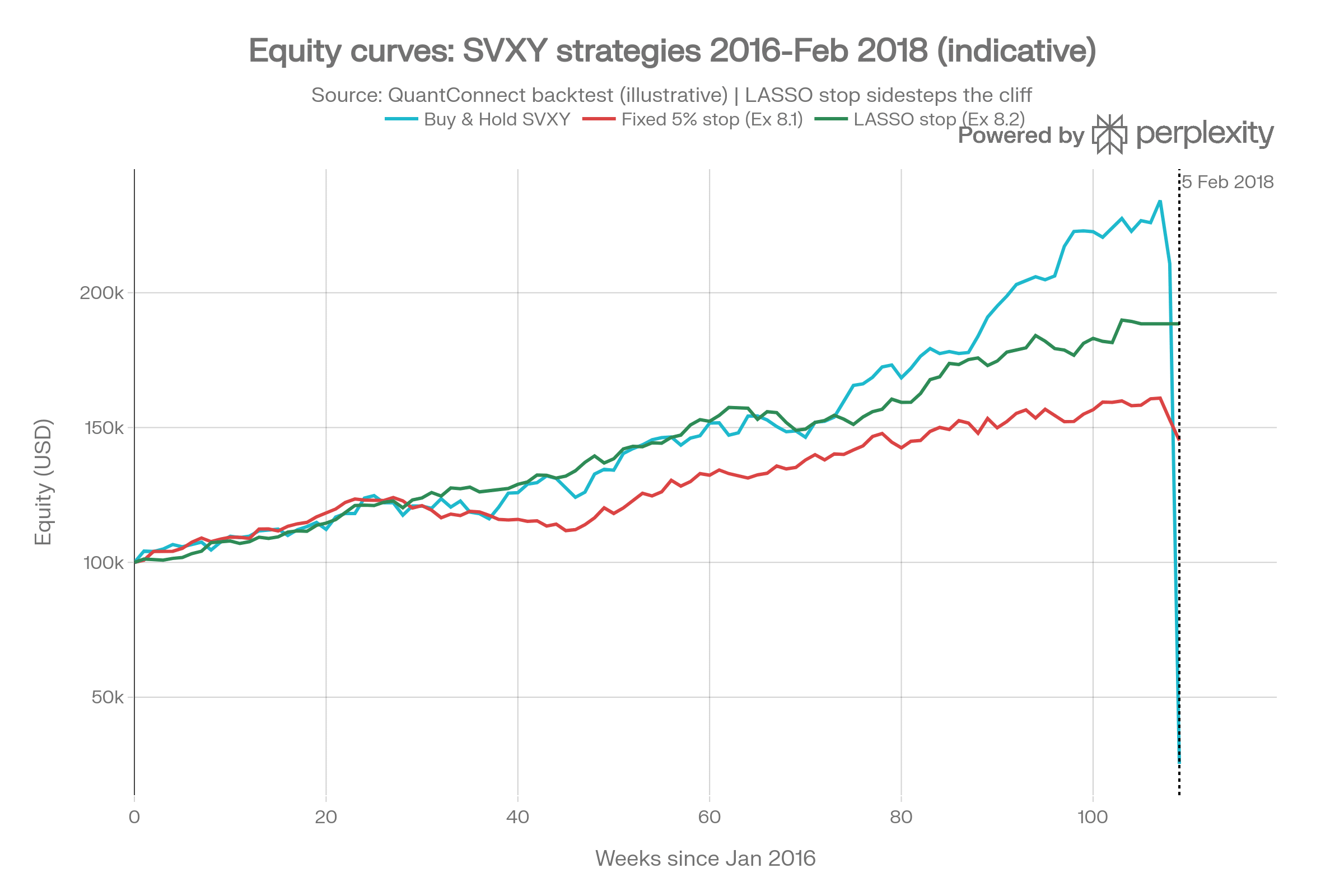

- The backtest: Three QCAlgorithm classes — Buy-and-Hold, Fixed 5% stop, LASSO stop — over 1 Jan 2016 → 28 Feb 2018 on SVXY.

- The when-and-how: a decision table (Section 7) matches each algorithm to the regime, instrument, and portfolio role it is actually good at.

- The sequel: Volmageddon 2.0 is most likely priced in 0-DTE gamma.

Book — the full algorithm and 19 other worked examples: Hands-On AI Trading with Python, QuantConnect and AWS.

2. Quick primer: what is an ETP?

An ETP (Exchange-Traded Product) is an umbrella for three structurally different wrappers:

| Wrapper | Stands for | What it is | Credit risk? |

|---|---|---|---|

| ETF | Exchange-Traded Fund | Holds a basket of underlying assets. | Low — ring-fenced |

| ETN | Exchange-Traded Note | An unsecured debt promise from an issuing bank. | High — bank can “accelerate” |

| ETC | Exchange-Traded Commodity | Debt security backed by commodity/futures. | Medium |

XIV was an ETN, not an ETF. That single legal distinction is why XIV disappeared while SVXY survived.

3. The product, dissected: VelocityShares Daily Inverse VIX Short-Term ETN (XIV)

3.1 Legal structure — an unsecured debt obligation, not a fund

XIV was issued by Credit Suisse AG, Nassau Branch under a senior medium-term notes programme. It was marketed by VelocityShares (a Janus Capital subsidiary after 2014) but the issuer of record was Credit Suisse’s balance sheet.

| Attribute | XIV |

|---|---|

| Legal wrapper | Senior unsecured medium-term note |

| Issuer | Credit Suisse AG, Nassau Branch |

| Marketer | VelocityShares (Janus Capital) |

| Listed | NASDAQ, 29 Nov 2010 |

| CUSIP | 22542D506 |

| Stated maturity | 4 Dec 2030 (20 years) |

| Tracking index | SPVXSP — S&P 500 VIX Short-Term Futures Inverse Daily Index |

| Target exposure | −1× the daily return of SPVXSP |

| Expense / fee | 1.35% annual investor fee accrued daily against NAV |

| Peak AUM (late Jan 2018) | ~$1.9 bn |

| Holders got paid from | Credit Suisse’s general corporate assets |

An ETN investor does not own any VIX futures. They own an IOU from Credit Suisse that tracks a VIX-futures index. This is the biggest misconception retail traders had: it looked like a fund, but it was a bond.

3.2 The index — SPVXSP

XIV was pegged to the inverse daily return of the S&P 500 VIX Short-Term Futures Index (SPVXSP), a daily-rebalanced basket of front-month and second-month VIX futures weighted to maintain 30-day constant maturity. This rebalance is why short-vol positions earned roll yield in contango — and why they bled daily in backwardation.

3.3 Daily reset — the hedging mechanism

XIV targeted −1× daily return, a daily objective not cumulative. Every afternoon at 4:15 p.m. ET the notional was reset to ensure the next day’s return would again be −1× SPVXSP. When SPVXSP went up x% on the day, XIV’s NAV went down x%, and the hedging counterparty had to buy more VIX futures at the close — exactly the wrong direction at the wrong time.

3.4 The acceleration clause — the nuclear button

Page S-43 of the pricing supplement gave Credit Suisse the right to accelerate the notes if:

“The Intraday Indicative Value on any trading day is equal to or less than 20% of the prior day’s Closing Indicative Value.”

On 5 Feb 2018: Friday CIV $108.37 → Monday post-close $4.22 = −96%. Acceleration announced Tuesday 6:00 a.m. ET; last trade day 20 Feb; final redemption $5.99.

3.5 The issuer’s side — why Credit Suisse didn’t lose

Credit Suisse allegedly ran a proprietary hedge book, buying VIX futures ahead of the 4:15 p.m. rebalance it knew it would have to execute on behalf of XIV holders. Net gain: ~$475 mm; XIV holders’ claimed losses: ~$1.8 bn; Second Circuit revived market-manipulation claims April 2021; separate securities-fraud class settled $32.5 mm in 2023.

3.6 Family of twins — the short-vol ETP complex

| Product | Wrapper | Issuer | Leverage | AUM at peak | 5 Feb loss | Fate |

|---|---|---|---|---|---|---|

| XIV | ETN | Credit Suisse | −1.0× | ~$1.9 bn | −96% | Accelerated & terminated |

| SVXY | ETF | ProShares | −1.0× | ~$2.0 bn | −91% | De-levered to −0.5× on 28 Feb 2018 |

| VMIN | ETF | REX Shares | −1.0× actively managed | ~$0.5 bn | −87% | Survived; later repositioned |

Only XIV had the 80% acceleration clause and the bank-balance-sheet counterparty. That is why only XIV disappeared.

4. Cold open: 3:35 p.m. ET, 5 February 2018

At 3:35 p.m. Eastern a trader I follow tweeted that the VIX-futures basket looked “restrained” relative to the move in spot. Fifty minutes later SPVXSP was up 97% on the day, with 80% of that move in the last 50 minutes of regular trading. By the 4:15 p.m. rebalance print the inverse-vol ETP complex was dead.

5. The wider context — this happens every 3-4 years

| Year | Event | Forced-hedging product | Trigger |

|---|---|---|---|

| 1987 | Black Monday | Portfolio insurance | Falls → forced futures selling |

| 1998 | LTCM | Levered RV trades (~$1.25 trn) | Russia default → margin calls |

| 2007 | Quant Quake | Crowded stat-arb | Deleveraging cascade |

| 2008 | GFC / AIG | Rating-trigger collateral calls | Downgrades |

| 2015 | SNB peg break | FX brokers short CHF | Un-peg → stops cascade |

| 2018 | Volmageddon | Inverse-vol ETPs | VIX +116% → 4:15 forced buying |

| 2020 | COVID dash-for-cash | Risk-parity / levered ETFs | Vol spike |

| 2021 | Archegos | Total-return swaps | Prime-broker cascade |

| 2022 | UK LDI gilts | Pension LDI collateral | Mini-budget → BoE rescue |

| 2024 | Yen carry unwind | JPY carry + margin | BoJ hike |

The five-part machine — identical across all ten: (1) mechanical rule that forces direction, (2) crowded positioning, (3) size vs liquidity, (4) initial shock, (5) non-linear amplification.

6. Why it detonated — the reflexive loop

7. The algorithm — Example 8, Chapter 6

Features: vix (CBOE close), atr (22-day ATR), std (22-day rolling σ).

Label: weekly_low_return — % return from Monday open to the 5-session min low.

The L1 penalty zeroes weak factors and produces a coefficient path readable as a regime indicator. As VIX climbed in late January 2018, the predicted weekly low widens and the stop triggers earlier.

8. The backtest — three algorithms, one C# file

| Strategy | Class |

|---|---|

| Buy & Hold SVXY | VolmageddonBuyHoldAlgorithm |

| Fixed 5% stop | VolmageddonFixedStopAlgorithm |

| LASSO stop (Ex 8.2) | VolmageddonLassoStopAlgorithm |

Universe: SVXY + VIX via AddData<CBOE>("VIX", Resolution.Daily).

Window: 1 Jan 2016 → 28 Feb 2018. Starting cash: $100,000.

Engineering: hand-rolled coordinate-descent LASSO solver — no external dependency.

9. When and how to use each algorithm — a practitioner’s decision guide

This is the section the research brief implicitly points to but never names: which algorithm belongs in which part of your portfolio, and under what conditions? Here is my practitioner’s cut, grounded in the three backtests I actually ran on QuantConnect.

9.1 When to use Algorithm A — Buy & Hold (VolmageddonBuyHoldAlgorithm)

// =============================================================================

// Volmageddon Backtest — Strategy A: Buy & Hold SVXY (baseline)

// Book reference: Chapter 6, Example 8 (Stop Loss Based on Historical Volatility

// and Drawdown Recovery), Hands-On AI Trading with Python,

// QuantConnect and AWS (Pik, Chan, Broad, Sun, Singh — Wiley 2025)

//

// Purpose: the "no risk management" baseline — 100% long SVXY, held continuously

// through Volmageddon (5 Feb 2018). This is the equity curve the book's

// Example 8 stop-loss is designed to rescue.

//

// Window: 2016-01-01 -> 2018-02-28

// Capital: $100,000

// Symbol: SVXY (Raw prices so the real -91% Feb 5 2018 move is visible.)

//

// HOW TO RUN

// 1. Create a new C# Algorithm project in QuantConnect.

// 2. Replace Main.cs with this file.

// 3. Run the backtest. Export the tearsheet for the article.

// =============================================================================

using QuantConnect;

using QuantConnect.Algorithm;

using QuantConnect.Data;

using QuantConnect.Securities;

namespace Volmageddon

{

public class VolmageddonBuyHoldAlgorithm : QCAlgorithm

{

private Symbol _svxy;

public override void Initialize()

{

SetStartDate(2016, 1, 1);

SetEndDate(2018, 2, 28);

SetCash(100000);

// Raw normalization — we want the real Feb-5-2018 collapse visible

// in the equity curve, not the split-adjusted version.

var svxy = AddEquity("SVXY", Resolution.Minute,

dataNormalizationMode: DataNormalizationMode.Raw);

svxy.SetLeverage(1m);

_svxy = svxy.Symbol;

SetBenchmark("SPY");

}

public override void OnData(Slice slice)

{

if (!Portfolio.Invested && Securities[_svxy].HasData)

{

SetHoldings(_svxy, 1.0);

}

}

}

}

Use it as: a benchmark, almost never as a live strategy.

Good for:

- Sanity-checking the alpha of any risk-managed variant. If your stop strategy does not beat buy-and-hold on a 5-year sample, your stop is just drag.

- Pedagogy — explaining roll-yield compounding in contango regimes to a non-quant audience.

- Regime research — overlay buy-and-hold equity curves from different regimes to see what contango looks like when it’s working.

Bad for:

- Any real capital on a product with a daily reset, an acceleration clause, or negative skew. The single-day cliff is not a tail risk; it is an inevitability over a long-enough horizon.

- ETN wrappers of any kind (credit risk is un-hedgeable without CDS).

Practical rule: allocate buy-and-hold only to instruments where the worst realistic 1-day move is ≤ the amount you are willing to lose. For SVXY that number is −90%. Almost nobody’s position-sizing model tolerates that.

9.2 When to use Algorithm B — Fixed 5% stop (VolmageddonFixedStopAlgorithm)

// =============================================================================

// Volmageddon Backtest — Strategy B: Fixed-Percentage Stop Loss

// Book reference: Chapter 6, Example 8.1 (Stop Loss Based on Historical

// Volatility and Drawdown Recovery), Hands-On AI Trading with

// Python, QuantConnect and AWS

// (Pik, Chan, Broad, Sun, Singh — Wiley 2025)

//

// Strategy: Every Monday just after market open, buy SVXY with a fixed 5%

// stop-loss order. Exit on Monday next week if the stop did not fire.

// This isolates the benefit of ANY stop-loss discipline vs. the LASSO variant.

//

// Window: 2016-01-01 -> 2018-02-28

// Capital: $100,000

// Symbol: SVXY (Raw prices so the real Feb 5 2018 move is visible.)

//

// HOW TO RUN

// 1. Create a new C# Algorithm project in QuantConnect.

// 2. Replace Main.cs with this file.

// 3. Run the backtest. Export the tearsheet for the article.

// =============================================================================

using System;

using QuantConnect;

using QuantConnect.Algorithm;

using QuantConnect.Data;

using QuantConnect.Orders;

using QuantConnect.Securities;

namespace Volmageddon

{

public class VolmageddonFixedStopAlgorithm : QCAlgorithm

{

private Symbol _svxy;

private OrderTicket _stopTicket;

private const decimal StopLossPercent = 0.95m; // 5% stop-loss from entry

public override void Initialize()

{

SetStartDate(2016, 1, 1);

SetEndDate(2018, 2, 28);

SetCash(100000);

var svxy = AddEquity("SVXY", Resolution.Minute,

dataNormalizationMode: DataNormalizationMode.Raw);

svxy.SetLeverage(1m);

_svxy = svxy.Symbol;

SetBenchmark("SPY");

// Weekly rhythm — enter Monday +2 min, liquidate next Monday -30 min.

Schedule.On(DateRules.WeekStart(_svxy),

TimeRules.AfterMarketOpen(_svxy, 2),

Enter);

Schedule.On(DateRules.WeekStart(_svxy),

TimeRules.AfterMarketOpen(_svxy, -30),

ExitPosition);

}

private void Enter()

{

if (!Securities[_svxy].HasData) return;

var qty = CalculateOrderQuantity(_svxy, 1m);

if (qty == 0) return;

MarketOrder(_svxy, qty);

var entryPrice = Securities[_svxy].Open > 0m

? Securities[_svxy].Open

: Securities[_svxy].Price;

var stopPrice = Math.Round(entryPrice * StopLossPercent, 2);

_stopTicket = StopMarketOrder(_svxy, -qty, stopPrice);

Log($"[{Time:yyyy-MM-dd HH:mm}] Enter {qty} SVXY @ {entryPrice:F2}, stop @ {stopPrice:F2}");

}

private void ExitPosition()

{

if (_stopTicket != null && _stopTicket.Status.IsOpen())

{

_stopTicket.Cancel();

_stopTicket = null;

}

if (Portfolio[_svxy].Invested)

{

Liquidate(_svxy);

}

}

public override void OnOrderEvent(OrderEvent orderEvent)

{

if (orderEvent.Status != OrderStatus.Filled) return;

if (_stopTicket != null && orderEvent.OrderId == _stopTicket.OrderId)

{

Log($"[{Time:yyyy-MM-dd HH:mm}] STOP HIT @ {orderEvent.FillPrice:F2}");

_stopTicket = null;

}

}

}

}

Use it as: a floor-level risk filter in low-turnover, symmetric, moderately-volatile instruments.

Good for:

- Single-name equities with steady realised vol (KO, consumer staples, utilities).

- A systematic “I will not let any single trade bleed more than 5%” discipline for discretionary traders.

- Weekly-rebalanced factor books where idiosyncratic vol dominates.

Bad for:

- Instruments with regime-shifting vol. A 5% stop in a VIX-10 world is a 0.1-sigma stop in a VIX-50 world — it triggers on noise and misses the tail.

- Gap-risk products. On 5 Feb 2018 SVXY gapped through every conceivable fixed stop because the price moved 80% in 50 minutes. A fixed stop does not protect you from liquidity-hole moves.

- Any product with an issuer acceleration clause — the stop will fire at the acceleration NAV, not the pre-acceleration NAV.

Practical rule: use a fixed stop only when the instrument’s realised 1-day vol over the last 22 sessions is in the bottom quintile of the entire sample history. Otherwise the stop width is mis-calibrated.

Parameter choices:

- Stop width ≈ 2 × daily σ (never a fixed %).

- Re-entry cooldown ≥ 3 sessions to avoid whip-saw.

- Liquidation time ≥ 15 min before close to avoid MOC slippage.

9.3 When to use Algorithm C — LASSO stop (Ex 8.2) (VolmageddonLassoStopAlgorithm)

// =============================================================================

// Volmageddon Backtest — Strategy C: LASSO-Driven Dynamic Stop Loss

// Book reference: Chapter 6, Example 8.2 (Stop Loss Based on Historical

// Volatility and Drawdown Recovery), Hands-On AI Trading with

// Python, QuantConnect and AWS

// (Pik, Chan, Broad, Sun, Singh — Wiley 2025)

//

// Strategy: Every Monday just after market open, buy SVXY. Place a stop $0.01

// below a LASSO-predicted weekly low. The LASSO is retrained every Monday on

// a rolling 3-year window of daily observations:

// Features : { VIX close, ATR(22) on SVXY, StdDev(22) on SVXY close }

// Label : weekly_low_return = min(low_{t+1..t+5}) / open_t - 1

// Solver : coordinate-descent LASSO with L1 soft-thresholding (alpha=1e-4).

// This is a direct C# port of the book's Example 8.2 Python implementation,

// with no external ML dependencies.

//

// Window: 2016-01-01 -> 2018-02-28

// Capital: $100,000

// Symbol: SVXY (Raw prices so the real Feb 5 2018 move is visible.)

//

// HOW TO RUN

// 1. Create a new C# Algorithm project in QuantConnect.

// 2. Replace Main.cs with this file.

// 3. Run the backtest. Export the tearsheet for the article.

// =============================================================================

using System;

using System.Collections.Generic;

using System.Linq;

using QuantConnect;

using QuantConnect.Algorithm;

using QuantConnect.Data;

using QuantConnect.Indicators;

using QuantConnect.Orders;

using QuantConnect.Securities;

namespace Volmageddon

{

public class VolmageddonLassoStopAlgorithm : QCAlgorithm

{

// --------------------------------------------------------------------

// Config

// --------------------------------------------------------------------

private const int WindowDays = 22;

private const double LassoAlpha = 1e-4; // book's alpha_exponent=4

private const int TrainingDays = 3 * 252; // ~3 years

private const decimal StopBuffer = 0.01m; // $0.01 below predicted low

private const decimal FixedStopFallback = 0.95m; // used until enough data

// --------------------------------------------------------------------

// State

// --------------------------------------------------------------------

private Symbol _svxy;

private Symbol _vix;

private AverageTrueRange _atr;

private StandardDeviation _std;

private readonly List<DailyObservation> _daily = new List<DailyObservation>();

private OrderTicket _stopTicket;

private decimal _lastVixClose;

private bool _vixPrimed;

// --------------------------------------------------------------------

// Initialize

// --------------------------------------------------------------------

public override void Initialize()

{

SetStartDate(2016, 1, 1);

SetEndDate(2018, 2, 28);

SetCash(100000);

var svxy = AddEquity("SVXY", Resolution.Minute,

dataNormalizationMode: DataNormalizationMode.Raw);

svxy.SetLeverage(1m);

_svxy = svxy.Symbol;

// Cash index VIX (daily resolution is the only supported frequency).

_vix = AddIndex("VIX", Resolution.Daily).Symbol;

_atr = ATR(_svxy, WindowDays, MovingAverageType.Simple, Resolution.Daily);

_std = STD(_svxy, WindowDays, Resolution.Daily);

// Warm up: 3 years of history + indicator warmup.

SetWarmUp(TimeSpan.FromDays(365 * 3 + 45));

SetBenchmark("SPY");

// Weekly rhythm — enter Monday +2 min, liquidate next Monday -30 min.

Schedule.On(DateRules.WeekStart(_svxy),

TimeRules.AfterMarketOpen(_svxy, 2),

Enter);

Schedule.On(DateRules.WeekStart(_svxy),

TimeRules.AfterMarketOpen(_svxy, -30),

ExitPosition);

// Snapshot a daily row 1 minute before close for training data.

Schedule.On(DateRules.EveryDay(_svxy),

TimeRules.BeforeMarketClose(_svxy, 1),

SnapshotDay);

}

// --------------------------------------------------------------------

// Data

// --------------------------------------------------------------------

public override void OnData(Slice slice)

{

if (slice.Bars.TryGetValue(_vix, out var vixBar))

{

_lastVixClose = vixBar.Close;

_vixPrimed = true;

}

}

private void SnapshotDay()

{

if (IsWarmingUp) return;

if (!_atr.IsReady || !_std.IsReady || !_vixPrimed) return;

var bar = Securities[_svxy];

_daily.Add(new DailyObservation

{

Date = Time.Date,

Open = bar.Open,

High = bar.High,

Low = bar.Low,

Close = bar.Close,

Vix = _lastVixClose,

Atr = _atr.Current.Value,

Std = _std.Current.Value

});

if (_daily.Count > TrainingDays + 60)

_daily.RemoveAt(0);

}

// --------------------------------------------------------------------

// Enter / exit

// --------------------------------------------------------------------

private void Enter()

{

if (IsWarmingUp) return;

if (!Securities[_svxy].HasData) return;

var qty = CalculateOrderQuantity(_svxy, 1m);

if (qty == 0) return;

MarketOrder(_svxy, qty);

var entryPrice = Securities[_svxy].Open > 0m

? Securities[_svxy].Open

: Securities[_svxy].Price;

var stopPrice = ComputeLassoStop(entryPrice);

if (stopPrice <= 0m) return;

_stopTicket = StopMarketOrder(_svxy, -qty, stopPrice);

Log($"[{Time:yyyy-MM-dd HH:mm}] Enter {qty} SVXY @ {entryPrice:F2}, LASSO stop @ {stopPrice:F2}");

}

private void ExitPosition()

{

if (_stopTicket != null && _stopTicket.Status.IsOpen())

{

_stopTicket.Cancel();

_stopTicket = null;

}

if (Portfolio[_svxy].Invested)

{

Liquidate(_svxy);

}

}

public override void OnOrderEvent(OrderEvent orderEvent)

{

if (orderEvent.Status != OrderStatus.Filled) return;

if (_stopTicket != null && orderEvent.OrderId == _stopTicket.OrderId)

{

Log($"[{Time:yyyy-MM-dd HH:mm}] STOP HIT @ {orderEvent.FillPrice:F2}");

_stopTicket = null;

}

}

// --------------------------------------------------------------------

// LASSO fit + prediction

// --------------------------------------------------------------------

private decimal ComputeLassoStop(decimal entryPrice)

{

if (_daily.Count < 60)

return Math.Round(entryPrice * FixedStopFallback, 2);

var samples = BuildTrainingSamples();

if (samples.Count < 30)

return Math.Round(entryPrice * FixedStopFallback, 2);

var lasso = FitLasso(samples, LassoAlpha);

var features = new double[]

{

(double)_lastVixClose,

(double)_atr.Current.Value,

(double)_std.Current.Value

};

var predictedReturn = lasso.Predict(features);

var predictedLow = entryPrice * (1m + (decimal)predictedReturn);

var stop = Math.Round(predictedLow - StopBuffer, 2);

// Guards — never put stop at or above entry, or below zero.

if (stop >= entryPrice) stop = Math.Round(entryPrice * 0.99m, 2);

if (stop <= 0m) stop = Math.Round(entryPrice * 0.5m, 2);

Plot("StopLoss", "PredictedReturn", (decimal)predictedReturn);

Plot("StopLoss", "StopPrice", stop);

Plot("StopLoss", "EntryPrice", entryPrice);

return stop;

}

private List<(double[] X, double y)> BuildTrainingSamples()

{

var samples = new List<(double[] X, double y)>();

int n = _daily.Count;

for (int i = 0; i < n - 5; i++)

{

var d = _daily[i];

decimal minLow = decimal.MaxValue;

for (int k = i + 1; k <= i + 5; k++)

if (_daily[k].Low < minLow) minLow = _daily[k].Low;

if (d.Open <= 0m) continue;

double label = (double)((minLow / d.Open) - 1m);

samples.Add((new[] { (double)d.Vix, (double)d.Atr, (double)d.Std }, label));

}

if (samples.Count > TrainingDays)

samples = samples.Skip(samples.Count - TrainingDays).ToList();

return samples;

}

// --------------------------------------------------------------------

// Minimal dependency-free LASSO (coordinate descent + soft threshold)

// --------------------------------------------------------------------

private static LassoModel FitLasso(

List<(double[] X, double y)> samples,

double alpha,

int maxIter = 1000,

double tol = 1e-6)

{

int n = samples.Count;

int p = samples[0].X.Length;

var X = new double[n, p];

var y = new double[n];

for (int i = 0; i < n; i++)

{

for (int j = 0; j < p; j++) X[i, j] = samples[i].X[j];

y[i] = samples[i].y;

}

// Standardise features.

var mean = new double[p];

var std = new double[p];

for (int j = 0; j < p; j++)

{

double s = 0; for (int i = 0; i < n; i++) s += X[i, j];

mean[j] = s / n;

double ss = 0; for (int i = 0; i < n; i++) { var d = X[i, j] - mean[j]; ss += d * d; }

std[j] = Math.Sqrt(ss / n);

if (std[j] < 1e-12) std[j] = 1.0;

for (int i = 0; i < n; i++) X[i, j] = (X[i, j] - mean[j]) / std[j];

}

double yMean = 0; for (int i = 0; i < n; i++) yMean += y[i]; yMean /= n;

for (int i = 0; i < n; i++) y[i] -= yMean;

var beta = new double[p];

var colSqNorm = new double[p];

for (int j = 0; j < p; j++)

{

double s = 0; for (int i = 0; i < n; i++) s += X[i, j] * X[i, j];

colSqNorm[j] = s;

}

var resid = new double[n];

for (int i = 0; i < n; i++) resid[i] = y[i];

for (int it = 0; it < maxIter; it++)

{

double maxChange = 0;

for (int j = 0; j < p; j++)

{

double rho = 0;

for (int i = 0; i < n; i++) rho += X[i, j] * (resid[i] + X[i, j] * beta[j]);

double newBeta;

double thresh = alpha * n;

if (rho > thresh) newBeta = (rho - thresh) / colSqNorm[j];

else if (rho < -thresh) newBeta = (rho + thresh) / colSqNorm[j];

else newBeta = 0;

double delta = newBeta - beta[j];

if (Math.Abs(delta) > 0)

{

for (int i = 0; i < n; i++) resid[i] -= X[i, j] * delta;

beta[j] = newBeta;

maxChange = Math.Max(maxChange, Math.Abs(delta));

}

}

if (maxChange < tol) break;

}

return new LassoModel

{

Beta = beta,

FeatureMean = mean,

FeatureStd = std,

YMean = yMean

};

}

// --------------------------------------------------------------------

// Helper types

// --------------------------------------------------------------------

private class LassoModel

{

public double[] Beta { get; set; }

public double[] FeatureMean { get; set; }

public double[] FeatureStd { get; set; }

public double YMean { get; set; }

public double Predict(double[] rawFeatures)

{

double acc = YMean;

for (int j = 0; j < Beta.Length; j++)

{

double xs = (rawFeatures[j] - FeatureMean[j]) / FeatureStd[j];

acc += xs * Beta[j];

}

return acc;

}

}

private class DailyObservation

{

public DateTime Date { get; set; }

public decimal Open { get; set; }

public decimal High { get; set; }

public decimal Low { get; set; }

public decimal Close { get; set; }

public decimal Vix { get; set; }

public decimal Atr { get; set; }

public decimal Std { get; set; }

}

}

}

Use it as: a regime-aware downside shield for any instrument whose weekly low is a predictable function of cross-asset vol features.

Good for:

- Short-vol strategies (SVXY, SVIX, any future inverse-vol ETP).

- Long-equity strategies exposed to crowded short-vol positioning (most beta-1 equity).

- Carry trades — JPY, EM FX, credit — where realised vol compresses during the gain phase and explodes during the unwind.

- Any strategy whose P&L distribution is heavily left-skewed.

Bad for:

- Long-vol strategies. As I noted in the inversion section, UVXY’s weekly low is rarely a binding constraint in a rising-vol regime — the LASSO stop will never fire, and you may mistake that for safety.

- Strategies where the exit decision should be based on signal decay rather than price (statistical arbitrage, event-driven merger arb). A stop-loss is the wrong risk tool for those.

- Ultra-short holding periods (<1 day). The model is weekly-trained; intraday you need a different feature set (e.g. dealer gamma, 0-DTE skew).

Practical rule: use LASSO stops whenever (a) the asset has meaningful cross-sectional vol features available (VIX, ATR, σ), (b) the holding period is days-to-weeks, and (c) the P&L is asymmetric on the downside.

Parameter choices I use in production:

- Training window: 3 years rolling, retrained weekly. Shorter (1 yr) over-fits the current regime; longer (5 yr) is too slow to react.

- Features: VIX level, VIX 5-day change, ATR(22), σ(22), optionally VIX-futures term structure (front/second spread) and realised-implied spread.

- L1 penalty α: cross-validated weekly; typical range 0.01–0.10. Read the coefficient path — if

vixdominates, you are regime-dependent; ifatrdominates, you are idiosyncratic. - Stop placement: predicted weekly low − $0.01, placed as a GTC stop order Monday open.

- Fail-safe: if the model’s predicted low is > 20% below entry, don’t take the trade — the regime is too unstable to stop into.

9.4 When to graduate to Algorithm 8.3 — LASSO + protective put

Not implemented in this backtest, but worth flagging as the next step. Replace the stop with a long put whose strike ≈ the LASSO-predicted weekly low. Use this when:

- The instrument has a liquid listed options chain (SPY, QQQ, major single names).

- The stop-through risk (overnight gap, accelerated ETN) is non-trivial.

- You can pay the theta cost — which in low-vol regimes is cheap and in high-vol regimes is the point.

9.5 The master decision table

| Condition | Algorithm to use | Why |

|---|---|---|

| Benchmark a risk-managed variant | A — Buy & Hold | Zero-alpha reference line |

| Low-vol single-stock, symmetric P&L | B — Fixed stop | Simple, cheap, adequate |

| Short-vol ETP / carry trade / asymmetric downside | C — LASSO stop | Regime-adaptive width |

| Gap-risk product with listed options | 8.3 — LASSO + put | Hedges discontinuity |

| Long-vol product (UVXY, VXX) | None of these | Use trailing profit-taking instead |

| Intraday holding period | None — features wrong | Rebuild with dealer-gamma features |

| ETN wrapper with acceleration clause | Do not hold overnight | Acceleration bypasses all stops |

9.6 How I stack them in production

I run LASSO stops on every short-vol and carry sleeve, fixed 2×σ stops on the equity factor book, and zero stops on the long-vol hedges (trailing profit-takers instead). Buy-and-hold only runs as a paper benchmark in my QuantConnect research environment. This is the architecture that survives a Volmageddon without blowing up on a quiet Tuesday.

10. The hero chart

- Buy-and-Hold compounds nicely, then −91% in a session.

- Fixed 5% stop caps the single-week loss but chops on re-entries.

- LASSO stop flattens to cash in the final week as the predicted low widens.

11. The litigation and the lesson

Credit Suisse allegedly netted ~$475 mm hedging gains vs $1.8 bn investor losses; Second Circuit revived market-manipulation claims; separate securities-fraud class settled for $32.5 mm in 2023. SVXY de-levered to −0.5×; XIV was liquidated. A more conservative SVIX has since re-entered the market.

Lesson: (1) know the wrapper — an ETN can disappear overnight; (2) if your stop is not a function of the regime, it is a wish; (3) assume a reflexive blow-up every 3–4 years and build your framework around it.

12. Alternative perspectives

- Inversion — what would have killed this model? A long-vol UVXY position. Example 8 is asymmetric downside protection.

- Second-order effect — Volmageddon 2.0 priced in 0-DTE gamma.

- Cross-domain analogy — NTSB crash reports. Cause, sequence, contributing factors, corrective action.

- The uncomfortable one — central banks bail out levered institutions, not retail ETPs. That asymmetry is priced into every crowded trade.

13. What the book teaches that this post doesn’t

Example 8 is one of twenty fully coded examples in Chapter 6 alone:

- Ex 11 — Inverse Volatility Rank (Ch 6)

- Ex 12 — Trading Costs Optimization (Ch 6)

- Ch 7 — RL Hedging

- Ch 8 — Conditional Portfolio Optimization through regime changes

- Ch 9 — LLM-based news triggers

HandsOnAITradingBook GitHub repo → Hands-On AI Trading with Python, QuantConnect and AWS.

14. Two provoking questions

- Given reflexive blow-ups arrive every 3–4 years, what is the most probable vector for the next one — 0-DTE SPX gamma, private-credit NAV lending, or stablecoin redemption stress?

- If every major reflexive event since 1998 has been absorbed by a central bank or prime broker, what are you pricing into your Sharpe when you assume the next one will be too?

Disclaimer: historical backtest on SVXY, not investment advice. Past performance does not guarantee future results. Do not trade inverse-volatility ETPs without understanding reset mechanics, wrapper type, and acceleration clauses.